Methodology

We construct several transparent net-zero scenarios for the global steel sector based on projected demand, the retrofits cycle for steel plants, availability of scrap, access to CCS disposal geology, and solar PV and excess hydroelectric power driving hydrogen based steel making.

A detailed description of our methodology is provided in the technical report. The project method is summarized here.

Facility Database – We establish a database of existing 2019 facilities in 94 countries that includes age and current processes for making steel. We then dynamically and geographically add clean recycled and primary production when a minimum threshold of demand is met, eventually having steel production in 133 countries. By far the largest portion of steel making is in east Asia, with 54% of global production in China. We also derive facility-level production, energy use and emissions. Our boundary for direct emissions includes all direct energy and process emissions that typically occur at integrated iron and steel mills. We do not include upstream emissions (from the production of iron ore, processing of scrap steel off-site, and embodied emissions associated with the purchase of oxygen, lime, electricity and heat inputs) or downstream secondary manufacturing.

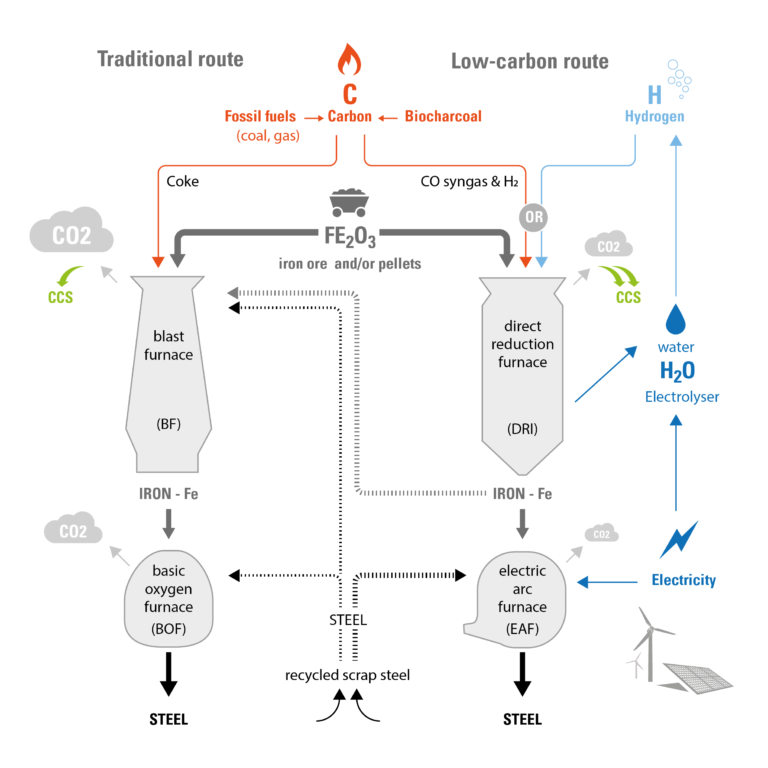

Decarbonization Options – We define deep decarbonization options for iron and steel production that will be incorporated into our pathways (Table 1 below). Given the needs for net-zero emissions economy wide by 2050, and based on the general practice of assessing CCS at -90% mitigation, we consider only options that are a maximum 10% of current emissions intensity. We do not consider the co-firing of BF-BOFs with hydrogen or the retrofit of BF-BOFs with CCS because these options only reach a 30-50% reduction in CO2 emissions.

Pathway Development – We project steel production demand to 2050 including material efficiency improvements, and then define how steel demand can be met through the retrofitting of current facilities and the building of new ones using deep decarbonization options using a transparent, algorithmic turnover of steel facilities to low emissions. This is based on estimates of each facility’s functional age since last build or last retrofit. Each facility is retrofit at the 25 year mark (we also test 32 and 40 years). We assume that carbon capture and storage (CCS) is preferable due to cost, and BFBOFs with CCS are preferable to syngas DRI EAFS because of familiarity of the industry with the BFBOF technology and its current ubiquity. Our allocation mechanism assumes:

- Carbon capture and storage (CCS) options are used when saline aquifer or depleted oil and gas wells are available nearby. Direct Reduced Iron with Carbon Capture and Storage (DRI-EAF-GAS-CCS), which is a currently commercial, is assumed until post combustion carbon capture and storage is mastered (BF-BOF-CCS ), assumed in 2030.

- If CCS is unavailable, we consider whether plentiful solar PV or excess hydropower are available at a reasonable cost to make electrolytic hydrogen for direct reduced iron (DRI-EAF-H2). Wind is not considered due to need for predictability for storage sizing.

If neither CCS nor solar PV/hydro generation are geospatially possible for existing production facilities, then “Non spatially allocated production” (NSP) is assumed. This could be new domestic or foreign new builds (as imports), or importation of green iron for use in EAFS.

In total we develop nine scenarios in order to consider three levels of long-term global steel demand and three lengths of available CO2 pipelines from existing sites. We also test the effect of longer retrofit cycles on the medium demand scenario. One assessment of scrap availability is used which allows for increased recycled steel use over time.

Steel production

The technical means to net-zero steel

- More material efficiency in the making of vehicles, buildings, and infrastructure

- More recycling of steel products. Depends on supply of reasonable quality scrap and a network to gather it, using Electric Arc Furnaces (EAF) + Direct Reduced Iron (DRI) “sweetening” to reduce contamination (Technology Readiness Level 9)

- Blast furnace Basic oxygen furnace (BF-BOF) with 90%+ Carbon capture and storage, possibly with biomass TRL 5* (2030?)

- Advanced smelting with CCS (Progress has slowed, not shown, TRL 7 acc to IEA)

- Syngas based DRI EAF with concentrated flow CCS TRL 9*. Replaceable with 100% green hydrogen

- Green hydrogen DRI EAF TRL 7+ (2028-’30)

- Molten oxide or aqueous oxide electrolysis TRL 4 (2035-’40?) Not in diagram.

* Clean hydrogen blending would allow partial reductions, but it was not used in this project due to partial reductions.

Table 1: Processes included in technology scenarios

Green shaded rows represent decarbonization options (EAF assumes green sources of electricity)

| Acronym | Name / Description | Use / Stage of Development |

| BF-BOF | Blast Furnaces for reducing iron ore / Basic Oxygen Furnaces for smelting | Widely used, 70% of global steel production. |

| DRI-EAF (GAS or COAL) | Direct Reduced Iron / Electric Arc Furnaces for smelting | 5% of global production |

| OHF | Open-hearth Furnace | Limited use, mostly replaced by BF-BOF |

| EAF | Electric Arc Furnaces | Widely used for smelting recycled scrap |

| BF-BOF-CCS (90%) | Blast Furnaces for reducing iron ore / Basic Oxygen Furnaces for smelting with 90% Post-combustion Carbon Capture and Storage | Advanced development stage (TRL 5) |

| DRI-EAF-GAS-CCS | Syngas direct reduced iron (DRI) with concentrated flow CO2 CCS followed by EAF | Fully commercial technology ready for market uptake (TRL 9). |

| DRI-EAF-H2 | Green hydrogen (electrolysis with clean electricity) DRI followed by EAF | Prototype Stage (TRL 5-7+). |